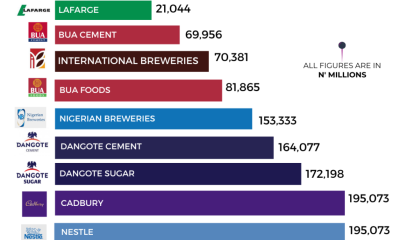

Some of Nigeria’s leading companies incurred a combined forex loss of N1.8 trillion in the financial year 2023. This is according to information contained in the...

The founder of Sustainable National Movement (SNM), Kayode Arimoro, has called on President Bola Tinubu to recall the suspended Minister of Humanitarian Affairs and Poverty Alleviation,...

The United States quietly sent long-range ballistic missiles to Ukraine as part of a package of military support in March, and Ukraine has already used the...

Nigeria’s Sports Minister, John Enoh has reportedly held talks with former Super Eagles head coach, Jose Peseiro over a possible return to the team. Peseiro left...

The Africa Youth Growth Foundation (AYGF) has urged the federal government to adopt Universal Health Coverage (UHC) to enable people access health care without financial restraint....

The presidential candidate of the Labour Party (LP) in last year’s general election, Peter Obi, has called for special interventions in Quranic learning for the almajiris,...

The Chartered Institute of Project Managers of Nigeria (CIPMN) has revealed that most projects in the country fail due to a lack of proper planning and...

To many supporters of the beautiful game, Lionel Messi is the best player to have ever laced up a pair of boots. The Argentinian was at...

Naija News looks at the top happenings making headlines on the front pages of Nigeria’s national newspapers today Thursday 25th April 2024. The PUNCH: Prices of...

Tupac Shakur’s estate is reportedly threatening to sue Drake over a recent diss track against Kendrick Lamar that featured an AI-generated version of the late rapper’s voice, calling it a...

A new poll by Quinnipiac University released Wednesday indicates that President Joe Biden’s slight lead over former President Donald Trump is vanishing. This happened despite Trump’s...

The United Nations (UN) has revealed that 22 per cent of decision-making positions are held by women in Nigeria’s private sector. Ms Beatrice Eyong, UN’s Women...

A Nigerian lady laments the hectic lifestyle in the United Kingdom (UK) as she packs her bag and returns to her home country with her family...

Former Manchester United forward Giuseppe Rossi has tipped club legend Roy Keane to take charge of the Premier League club. He feels the Man United legend...

Dana Air has announced that it is processing refunds for flights affected by its recent temporary suspension. The Nigeria Civil Aviation Authority (NCAA) imposed the suspension...

With Nigeria’s sustainable investment opportunities in the blue and green economies valued at over $100 billion annually, unlocking this potential remains critical to boosting the nation’s...

The Kano State Government has said that the current water scarcity being experienced in some part of the metropolis would soon be over, as it deployed...

Singer, Davido’s logistics manager, Israel Afeare, aka Israel DMW, has reacted after a doctor advised men to marry virgins. The doctor on X gave reasons...

The Federal Government has revoked 924 inactive mining licenses, alleging that miners have facilitated a black market for acquiring mining titles. The revoked licenses comprise 528...

President Bola Ahmed Tinubu has reaffirmed his administration’s commitment to tackling maternal mortality through dedication to the welfare and empowerment of women and young people across...