If African governments work together under AfCFTA, they can set the terms of engagement, ensuring that investors play by Africa’s rules, not the other way around. If we continue business as usual, our children will inherit holes in the ground, public health crises, unending conflict, and missed opportunities. But if African leaders rise to the occasion, Africa can become a global leader in the renewable energy industry, dictating prices rather than accepting whatever is offered.

As the world accelerates the transition from fossil fuels to clean energy, Africa is taking on a more strategic role in that transition due to the abundance of critical minerals within the continent. Africa boasts significant reserves of the world’s critical minerals, such as cobalt, manganese and lithium, which are essential for the production of electric vehicles, wind turbines, solar batteries, etc. The increased importance of these minerals has driven demand for them in recent years, which is projected to keep rising. According to the International Energy Agency, demand for lithium rose by 30 per cent in 2023, while demand for nickel, cobalt, graphite and rare earth elements all saw increases ranging from 8 per cent to 15 per cent. The projections are that demand for these minerals will double by 2030 and even triple by 2040.

According to UNCTAD, Africa has 55 per cent of the world’s cobalt reserves, 47 per cent of manganese, 21 per cent of graphite, 5.9 per cent of copper, and 5 per cent of nickel. This resource abundance places the continent at the centre of an emerging global contest. Nations and corporations from around the world now seek access to Africa’s mineral wealth, and this global race to secure supply of these minerals has a range of economic and political implications for the continent.

Foreign Investment and the Risk of Extractive Models

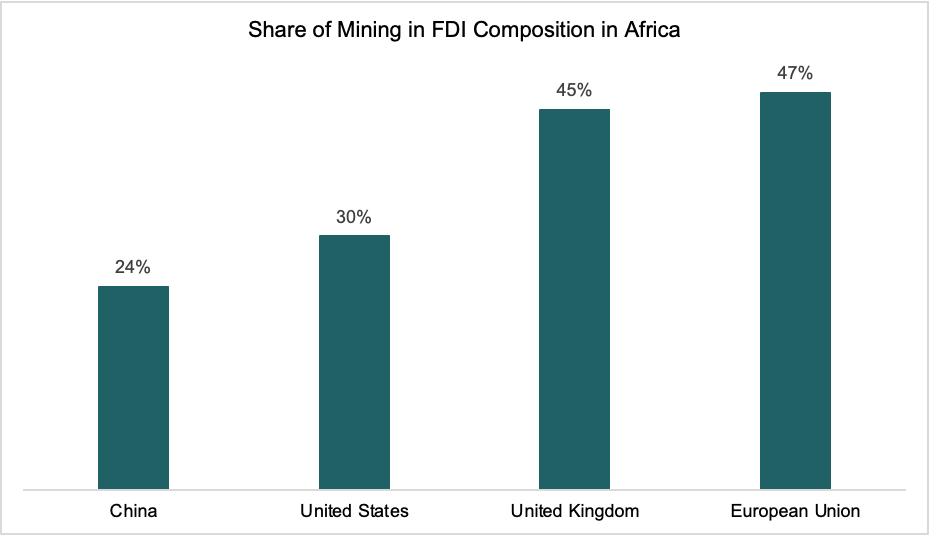

China has established itself as a force to be reckoned within Africa’s mining sector through significant investments across the continent, giving it ownership of 21 per cent of Africa’s mining sites and securing long-term contracts for the supply of these minerals. Chinese investment in Africa’s mining sector has risen over the past years to US$9.76 billion by 2022, representing 23.8 per cent of China’s total foreign direct investment FDI) stock in Africa.

Source: David Luke, The key to better trade with Africa (2023).

Nigerians need credible journalism. Help us report it.

Support journalism driven by facts, created by Nigerians for Nigerians. Our thorough, researched reporting relies on the support of readers like you.

Help us maintain free and accessible news for all with a small donation.

Every contribution guarantees that we can keep delivering important stories —no paywalls, just quality journalism.

However, as much as China’s investment in African mining is on the rise, it still pales in comparison to the level of investment from other blocs such as the United States, United kingdom or the European Union, as shown above. For the European Union, nearly half (47 per cent) of its FDI in Africa goes into mining; similarly, 45 per cent of the UK’s total FDI stock in Africa is concentrated in the mining sector as well.

However, China’s inroads in the sector is one to watch out for as it is also the largest buyer of African minerals, having imported about a third of Africa’s minerals and metals exports worth US$16.6 billion in 2020. The European Union, in response to China’s growing influence has leveraged initiatives like its Critical Raw Materials Act and the Global Gateway to mobilise investments to the tune of €300 billion to reduce Europe’s dependence on China and secure sustainable supply of these minerals for its industries.

On the other hand, the United States, through the Minerals Security Partnership, has committed significant resources to secure supply chains for critical minerals. The US has committed about $4 billion to the lobito corridor, a massive infrastructure project which connects the largest mining provinces of DRC, Zambia and Angola to the Atlantic Ocean, paving the way for access to Africa’s critical minerals and increased trade in these minerals westward — an alternative to China.

African nations seem to have woken up to the challenge of value addition. Within the past three years, a number of African countries, including Nigeria, Ghana, Namibia and Zimbabwe, have placed restrictions on the export of raw critical minerals. This is in a bid to strengthen mineral processing capabilities on the continent. Nigeria just launched its largest lithium processing plant, a $100 million facility with a processing capacity of 4,000 tonnes per day, established by Chinese company, Avatar Energy.

This evident geopolitical contest puts African countries in a difficult position. While foreign investments provide the much-needed infrastructure and capital, they risk perpetuating a colonial-style extractive model, where Africa continues to export its raw materials and high-value processing only takes place abroad.

Changing the Narrative through the AfCFTA

As this global race for critical minerals intensifies, Africa has an opportunity to change the narrative. For a continent holding 30 per cent of the world’s critical minerals, Africa only captures 10 per cent of value from these minerals, majorly because processing takes place outside the continent. A number of factors contribute to this, but mostly because Africa lacks the right policies, financial resources and infrastructure to drive value addition and trade. This is where the African Continental Free Trade Area (AfCFTA) comes in. The AfCFTA presents a potential alternative, an opportunity for Africa to redefine its role in the global economy by strengthening critical minerals supply chains and driving consequential intra-continental trade.

Much has been said on how the AfCFTA provides an umbrella for harmonisation of trade policies and the possibility for lower tariffs on the continent, which will make trade more valuable. Harmonised trade policies will mean that companies do not have to deal with a multiplicity of conflicting laws and procedures to do business across the continent. If a Ghanaian company wants to sell lithium batteries to Nigeria, for instance, they would not have to worry about unexpected taxes, additional documentation and unnecessary border delays because both countries have adopted similar trade policies.

The AfCFTA could also mean lower tariffs, which would make trade in the critical minerals value chain cheaper across Africa. This means that if a company that has mined lithium in Nigeria wants to sell to a processing factory in Rwanda, the lithium won’t become too expensive on reaching Rwanda, making that trade a profitable one for all involved.

African nations seem to have woken up to the challenge of value addition. Within the past three years, a number of African countries, including Nigeria, Ghana, Namibia and Zimbabwe, have placed restrictions on the export of raw critical minerals. This is in a bid to strengthen mineral processing capabilities on the continent. Nigeria just launched its largest lithium processing plant, a $100 million facility with a processing capacity of 4,000 tonnes per day, established by Chinese company, Avatar Energy. Another Chinese company has also announced a $200 million investment for another lithium factory in Nigeria.

Ghana is also looking to scale up its lithium processing and battery manufacturing, having granted Australia-based Atlantic Lithium a licence to mine lithium in 2023. US-based ReElement Technologies has also announced plans to build a $200 million processing facility in Ghana, with a capacity for 30,000 tonnes of battery-grade lithium carbonate per year. DRC and Zambia also entered into a partnership in 2022 to develop an EV battery supply chain, leveraging their extensive reserves of copper and cobalt.

These are steps in the right direction and AfCFTA can help scale these national efforts into a coordinated and even stronger regional value chain, pooling resources together for consequential processing and value addition. Raw critical minerals can move across countries easier and countries can leverage each other’s strengths and comparative advantage in extraction, processing and manufacturing. For example, Mali can mine lithium and refine it in Ghana’s processing facilities, while Nigeria’s processing capacity could serve neighbouring countries. This increases intra-African trade and reduces the level of dependence on global powers like the US, China or EU, ultimately strengthening Africa’s position in the global clean technology value chain.

The solution lies in regional cooperation and smart policy choices. Instead of competing for short-term foreign deals, African nations must align their industrial policies, ensuring that tax incentives, local content laws, and export duties push for refining and manufacturing within Africa. The export restrictions on critical minerals is a way to go, and that must be complemented with consistent action to ensure that these industries are built within the continent.

Cooperation Over Competition

One may argue that this is much easier said than done and that may be right, because African nations have often chosen to compete instead of cooperate. In this case, when the whole world is looking to Africa to supply these critical minerals, there might be pressure to prioritise quick revenue over long-term regional industrialisation.

Many African governments already rely on bilateral deals with China, the European Union, and the United States. For instance, China has bilateral partnerships with eleven African countries, and most of these partnerships appear to be “infrastructure-for-resources” agreements, as part of its Belt and Road Initiative (BRI) (Ndegwa, 2023). The consequence of these types of partnerships is that over 75 per cent of Africa’s mineral exports go to non-African countries, with China alone accounting for more than 40 per cent of the continent’s cobalt and lithium exports. This is a problem that must be solved and the AfCFTA can only solve that with regional cooperation. Without strong regional cooperation, AfCFTA could just become another arena where African nations compete for foreign investments, rather than collaborate on value addition.

Africa is indeed at an inflection point: continue exporting raw critical minerals for pennies on the dollar or take control of its destiny by processing, refining, and manufacturing within the continent. AfCFTA is more than just a trade deal; it is Africa’s chance to break free from centuries of being a mere supplier of raw materials to global powers. Think of it using the case of cocoa in Ghana. Despite being one of the world’s top producers, Ghana makes far less from exporting raw cocoa beans than Switzerland does from selling chocolate. The same story is unfolding with lithium, cobalt, and rare earth minerals. Without bold and coordinated action, Africa will keep fuelling the green energy transition abroad, while remaining stuck in poverty.

The solution lies in regional cooperation and smart policy choices. Instead of competing for short-term foreign deals, African nations must align their industrial policies, ensuring that tax incentives, local content laws, and export duties push for refining and manufacturing within Africa. The export restrictions on critical minerals is a way to go, and that must be complemented with consistent action to ensure that these industries are built within the continent.

Regional blocs like ECOWAS should establish common negotiating frameworks, ensuring that mineral-rich nations do not get stuck in a “race to the bottom” situation where countries engage in unhealthy competition by offering excessive tax breaks or loose environmental regulations to attract investment. Instead, a well-coordinated regional strategy can ensure that investments are distributed efficiently, maximising economic benefits, while promoting fair labour and environmental standards.

If African governments work together under AfCFTA, they can set the terms of engagement, ensuring that investors play by Africa’s rules, not the other way around. If we continue business as usual, our children will inherit holes in the ground, public health crises, unending conflict, and missed opportunities. But if African leaders rise to the occasion, Africa can become a global leader in the renewable energy industry, dictating prices rather than accepting whatever is offered. The world is rushing to secure Africa’s critical minerals, will Africa negotiate from a position of strength, or will it once again be a spectator in its own story? The choice is clear.

Ifeanyi Chukwudi leads the Development Programme at the Centre for Journalism Innovation and Development (CJID).

Support PREMIUM TIMES' journalism of integrity and credibility

At Premium Times, we firmly believe in the importance of high-quality journalism. Recognizing that not everyone can afford costly news subscriptions, we are dedicated to delivering meticulously researched, fact-checked news that remains freely accessible to all.

Whether you turn to Premium Times for daily updates, in-depth investigations into pressing national issues, or entertaining trending stories, we value your readership.

It’s essential to acknowledge that news production incurs expenses, and we take pride in never placing our stories behind a prohibitive paywall.

Would you consider supporting us with a modest contribution on a monthly basis to help maintain our commitment to free, accessible news?

TEXT AD: Call Willie - +2348098788999

English (US) ·

English (US) ·